The Raise That Shrinks Before You Spend It

Social Security Was Supposed To Keep Up With Inflation. So, Why Does It Feel Like Retirees Keep Losing Ground?

Social Security recipients got a 2.8% “raise” this year. Inflation’s running hotter than that. Energy costs jumped. Gas prices climbed. Medicare takes its cut before retirees even touch the damn money. According to federal inflation data, prices rose 3.3% year-over-year in March. So let’s ask the obvious fucking question: if your cost-of-living adjustment loses to the actual cost of living, what exactly are we calling this — a raise or paperwork with better PR?

Because here’s what nobody likes saying out loud: a lot of retirees are staring at this year’s COLA the same way you stare at twenty bucks somebody hands you after quietly borrowing fifty from your wallet.

Technically, money changed hands.

Functionally? You’re still behind.

And before somebody fires up Facebook to scream about lazy seniors expecting yachts and shrimp towers, calm the fuck down. Nobody’s asking for luxury. The argument’s simpler than that: if the government says Social Security is protected from inflation, shouldn’t the protection actually keep up with inflation?

That seems like a pretty low fucking bar.

The part that’ll really piss you off is how this thing actually works.

Most people hear “cost-of-living adjustment” and assume the government measures what retirees spend money on and adjusts checks accordingly. Sounds reasonable. Sounds logical. Sounds like something designed by people who’ve met an actual retired person.

Nope.

The formula behind Social Security COLAs uses CPI-W, a measure built around the spending patterns of urban wage earners and clerical workers — people still in the workforce. Not retirees. Not seniors spending a bigger share of their money on prescriptions, healthcare, utilities, insurance, and the kind of grocery bill that now feels like you accidentally wandered into a luxury boutique for eggs.

Right out of the gate, the system starts getting weird.

The government is effectively measuring inflation for retirees using spending habits that don’t fully reflect retiree life.

That matters.

Because retirees don’t experience inflation the same way a thirty-five-year-old office worker does. If gas spikes, utilities rise, prescriptions jump, or healthcare creeps higher, people on fixed incomes feel it fast.

There’s another inflation measure — CPI-E — meant to better reflect older Americans’ spending patterns.

Congress knows this shit.

Congress has known this shit.

And somehow the math still sits there broken while lawmakers move with all the urgency of a sloth buffering on motel Wi-Fi.

Meanwhile, retirees are left standing in checkout lines, wondering whether somebody replaced reality with a prank.

Quick detour: if you’re not subscribed, you’re reading this the hard way. No sponsors. No corporate babysitters. Just receipts and unfiltered analysis.

Then there’s the timing problem, which somehow makes this mess even dumber.

The COLA retirees got this January wasn’t based on prices today. It was based on inflation measured months earlier. Which means the raise lands after costs have already started sprinting ahead.

Inflation doesn’t politely pause while Washington updates spreadsheets.

By the time the adjustment arrives, retirees are often already absorbing higher costs in real time.

That’s why you keep hearing some version of the same sentence from older Americans:

“I’m getting by, but it’s tighter.”

That sentence should scare the shit out of people.

For millions of Americans, Social Security isn’t extra spending money. It is the money. There’s no magical side hustle waiting in the wings for somebody pushing eighty with arthritis. You don’t suddenly become a crypto influencer called Grandpa Diamond Hands and outrun prescription costs through hustle culture.

You cut back.

You skip little things.

Sometimes you skip things you probably shouldn’t.

And slowly, quietly, life shrinks.

Somebody reading this right now is already muttering, “Fine. But whose fault is inflation?”

Fair question.

Reality’s annoying here.

Presidents don’t control prices with a giant dial hidden under the Oval Office desk labeled MAKE EGGS NORMAL AGAIN. Energy prices move because of global markets, refinery bottlenecks, wars, supply disruptions, shipping costs, investor expectations, and markets generally behaving like caffeinated raccoons fighting over garbage.

But policy choices matter too.

They shape incentives. They affect costs. They influence how painful inflation becomes and how quickly prices settle down. Critics argue that some decisions involving trade, energy, or pressure around interest rates may worsen the price pressures consumers feel directly. Others argue inflation is driven mostly by global disruptions and structural forces bigger than any administration.

Economists can argue over spreadsheets until somebody throws a chair.

Retirees still have to buy groceries.

They experience inflation standing at the pharmacy counter, wondering why a refill suddenly costs more than expected. They experience it at the gas pump. At the checkout line. At the kitchen table with a calculator and a muttered, “Jesus Christ.”

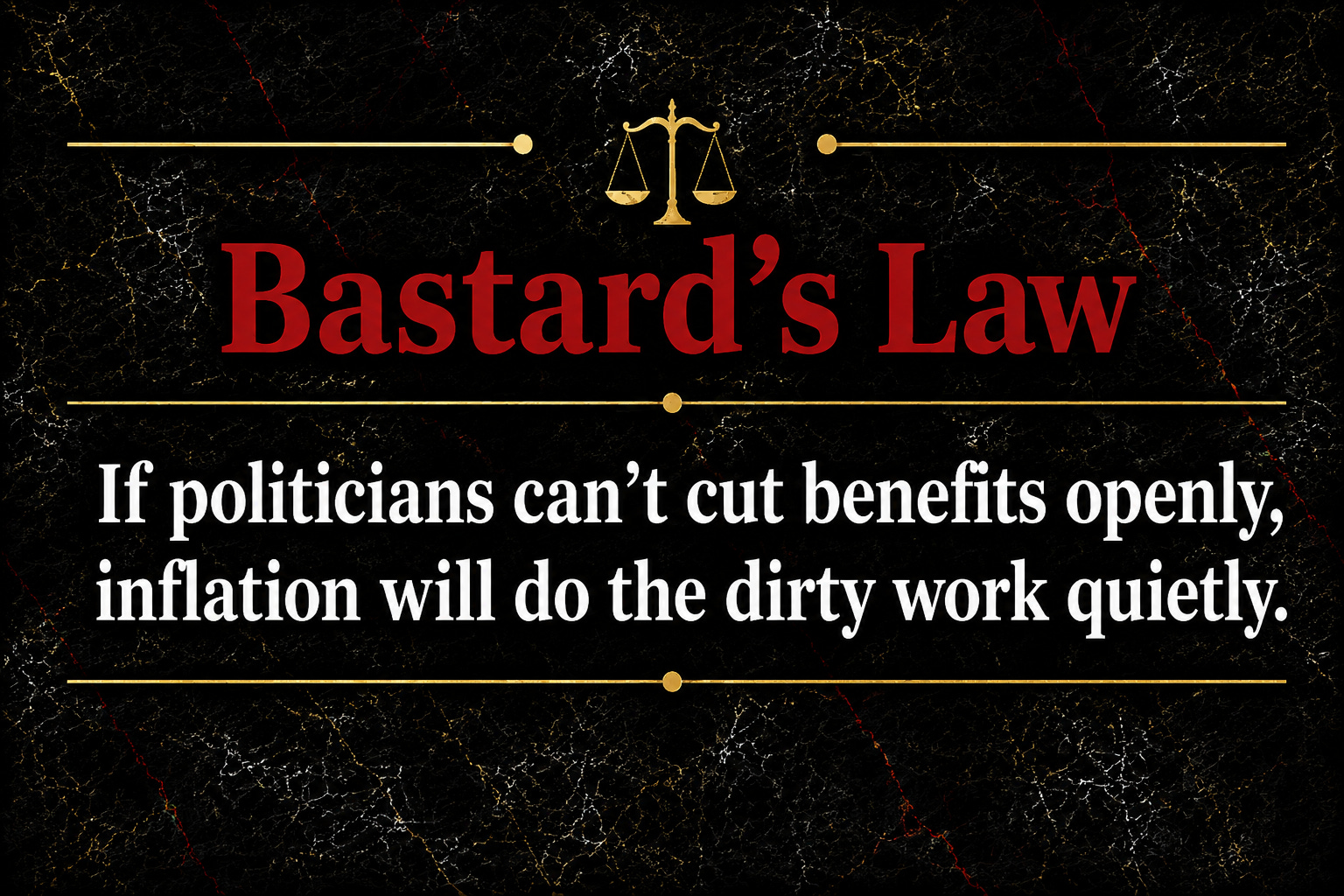

Here’s where this shit gets convenient for politicians:

Nobody wants to openly cut Social Security.

That’s political suicide.

Nobody wants the campaign ad featuring Grandma eating half a can of soup in the dark while a narrator says, “Congress chose fiscal discipline.”

So nobody says the quiet part out loud.

Nobody announces shrinking benefits.

Instead, benefits can lose buying power quietly.

A lagging formula here.

An adjustment that arrives late there.

A measurement that may not fully reflect retiree costs.

Death by a thousand bureaucratic paper cuts.

That’s the scandal.

Not that inflation exists.

Inflation happens.

The scandal is calling it a raise while retirees keep wondering why they’re somehow working harder just to stay in the same damn place.

And eventually something bigger breaks.

Trust.

Because institutions start losing credibility when official reality stops matching lived reality.

If headlines say inflation is easing while seniors feel squeezed every damn week, people stop trusting the explanation. Then they stop trusting the people explaining it.

Retirees don’t need motivational speeches or economists talking to them like confused toddlers.

They need math that resembles the world they actually live in.

Because a raise that arrives late, trails rising costs, and may not fully reflect how retirees actually spend money, doesn’t feel like protection.

It feels like paperwork wrapped in patriotic branding and handed over with a smile.

Upgrade

I’m retired. This is reader-funded. No sponsors. No corporate leash. No one telling me to tone it down.

Paid subscribers get bonus rants, full archive access, priority Q&A, and deeper dives that don’t make it into the free feed.

Upgrade and support independent work that doesn’t play nice.

If you want the same reality with a quieter voice and sharper claws, go check out Lotus Purrspective.

That’s where the judgment is calmer, cleaner, and somehow even more brutal.

Buy Me A Coffee

If this hit, consider supporting the work because yelling “what the fuck are we doing?” at the news doesn’t pay for itself.

#SocialSecurity #Inflation #Retirement #COLA #Economy #Seniors #CostOfLiving #TheUnredactedBastard